Highlights

-

Manatee County shifted into a more seller-leaning position in June 2026 as sales rose and inventory declined.

-

Pricing improved from last year, with both the median and average sale price moving higher.

-

Supply tightened more than it did in Sarasota County, giving sellers a stronger countywide position.

-

Homes sold faster than last year, which points to better buyer activity and stronger absorption.

-

Buyers still had choices, but the market became more competitive for well-priced homes.

Market Conditions

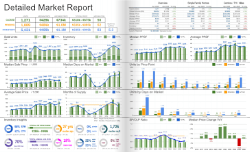

Manatee County showed clear improvement in June 2026. The county moved from a more balanced to buyer-leaning market last year into a balanced to seller-leaning market this year. The shift was driven by more sales, fewer active listings, and a lower supply level.

Closed sales increased to 1,161 in June 2026, up from 944 in June 2025. That was a strong year-over-year gain and nearly matched Sarasota County’s closed sales volume. Inventory declined to 3,974 homes, down from 4,662 one year earlier. With more demand moving through the market and fewer homes available, months of supply fell from 5.3 months to 3.8 months.

That 3.8-month supply level gives Manatee County a slightly tighter profile than Sarasota County, which had 4.2 months of supply. The difference is not extreme, but it matters. Manatee County buyers had fewer choices relative to demand, while sellers faced less direct competition than they did one year earlier.

Pricing Trends

Pricing strengthened in Manatee County in June. The median sale price rose to $444,000, up from $405,000 last June. Because the median reflects the middle of the market, this points to a meaningful improvement in the typical sale price.

The average sale price also increased, rising to $575,000 from $524,000 one year earlier. Since the average price can be influenced by higher-priced and luxury sales, this suggests that Manatee County benefited from both stronger typical pricing and a healthier mix of upper-end closings.

The median and average price increases moved in the same direction, which gives the pricing trend more support. This does not mean every segment appreciated equally, but it does show that pricing conditions were stronger than they were in June 2025.

Inventory Trends

Inventory declined across Manatee County, helping shift the market back toward sellers. Active listings fell from 4,662 in June 2025 to 3,974 in June 2026. That reduction eased seller competition and gave buyers fewer alternatives.

Months of supply dropped from 5.3 months to 3.8 months. This is one of the clearest signs that market balance improved. A supply level under 4 months is not as tight as the pandemic-era market, but it usually gives sellers more leverage when buyer activity is also rising.

Inventory conditions were not uniform across the county. East Manatee and North Manatee remained active, while the Manatee Keys and luxury market still carried more supply. This means some areas were more competitive than others, and pricing strategy still depended heavily on location and price point.

Market Pace

The pace of the Manatee County market improved in June. Median days on market fell to 46 days, down from 57 days one year earlier. Homes were not selling as quickly as they did during the peak years, but buyers were moving faster than they were last June.

The improvement in both closed sales and days on market points to stronger demand. Buyers were more willing to act when homes were priced correctly, especially in areas with tighter supply and good value compared with Sarasota County.

Even with that faster pace, the market still required discipline. Buyers were not chasing every listing, and sellers who priced ahead of the market could still face longer selling times. The strongest results likely came from homes that matched current buyer expectations on price, condition, and location.

What This Means for Buyers

Manatee County buyers had less leverage than they did last year, especially in areas where inventory tightened and sales improved. Well-priced homes could attract faster interest, so buyers needed to be prepared and realistic when strong listings appeared. There was still room to compare options, but the best opportunities required quicker decisions.

What This Means for Sellers

Manatee County sellers entered a stronger market than they faced in June 2025. Lower inventory, higher sales, and faster market times created better conditions for properly priced homes. Sellers still needed to avoid overpricing, especially in higher-supply segments, but the countywide market gave them a firmer position than last year.