Highlights

-

Sarasota County moved closer to balance in June 2026 as sales improved and inventory declined from last year.

-

Pricing held firm, with the median sale price rising modestly and the average price remaining elevated.

-

Inventory remained above the tightest years of the market, but supply was less burdensome than it was in June 2025.

-

Buyer activity improved, though homes still took longer to sell than they did during the pandemic-era market.

-

Sellers had a stronger position than last year, but accurate pricing remained essential.

Market Conditions

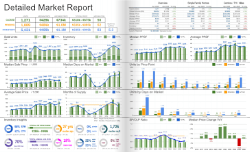

Sarasota County showed a more stable housing market in June 2026. Conditions improved from last year because sales rose, inventory declined, and months of supply moved back toward a more balanced range. The market was not broadly seller-dominated, but it was less buyer-leaning than it was in June 2025.

Closed sales increased to 1,173, up from 994 one year earlier. That gain shows stronger completed buyer activity across the county. Active inventory fell to 4,769 homes, down from 5,940 in June 2025. As a result, months of supply dropped from 5.8 months to 4.2 months.

A 4.2-month supply level points to balanced conditions with some seller advantage, especially when sales are rising. Buyers still had meaningful choice, but they had less leverage than they did when inventory was higher last year. Compared with the region overall, Sarasota County was slightly more supplied than Manatee County, but still much healthier than it was in June 2025.

Pricing Trends

Sarasota County pricing was steady to slightly stronger in June. The median sale price rose to $440,000, up from $430,000 last year. Because the median reflects the middle of the market, this suggests modest improvement in typical sale prices rather than a dramatic shift.

The average sale price increased to $687,000, up from $661,000 one year earlier. The higher average price shows continued strength in the upper end of the Sarasota County market, including luxury and waterfront-influenced sales. Since the average price is much higher than the median, sales mix remains an important part of the pricing story.

Together, the median and average price trends point to a market that is holding value but not accelerating quickly. Sarasota County pricing remained supported, but buyers were still selective and were not rewarding every listing equally.

Inventory Trends

Inventory declined meaningfully from last year, which changed the balance of the market. Active listings fell from 5,940 in June 2025 to 4,769 in June 2026. That reduction eased seller competition and gave the market a firmer footing.

Months of supply fell from 5.8 months to 4.2 months. This is important because Sarasota County moved from buyer-leaning territory closer to balance. Inventory was still far above the extreme shortage of 2021, when supply was below one month, but it no longer looked as elevated as it did last year.

The county’s inventory picture also varied by area. South Sarasota County and East Sarasota looked tighter than several coastal and luxury submarkets, while the Sarasota Keys, West Sarasota & Downtown, and the luxury segment still carried higher supply levels. That means sellers in some areas faced more competition than countywide numbers alone suggest.

Market Pace

The market pace improved, but it remained more normal than fast. Median days on market fell to 54 days, down from 61 days in June 2025. Buyers were moving faster than last year, but they were not acting with the urgency seen during 2021 and 2022.

The increase in closed sales supports that improvement. More homes sold even as inventory declined, which points to better buyer engagement. Still, a median market time of nearly two months shows that buyers continued to compare options and push back on pricing that did not match condition, location, or value.

This creates a market where strong listings can perform well, but weak pricing is still exposed. Sellers gained leverage from lower supply, but buyers retained enough choice to be selective.

What This Means for Buyers

Sarasota County buyers had less inventory than they did last year, so the best-priced homes required more decisive action. The market still offered choice, especially in higher-supply areas, but buyers could not assume every seller would be under pressure. Strong preparation and clear pricing comparisons were important before making an offer.

What This Means for Sellers

Sellers had a better market than they did in June 2025, with more sales activity and less competition from other listings. Even so, Sarasota County was not an automatic seller’s market. Accurate pricing, strong presentation, and realistic expectations remained important, especially in luxury, waterfront, and higher-inventory submarkets.